Monetary policy

2.1 European Central Bank revises monetary policy strategy

The principal changes in the new monetary policy strategy concern the price stability definition and the ECB’s inflation target. The new strategy adopts a symmetric inflation target of 2% over the medium term.

The Governing Council of the European Central Bank (ECB) revised the ECB’s monetary policy strategy in 2021. The ECB’s monetary policy strategy is based on the Treaty on the Functioning of the European Union and the mandate set out within it. The ECB’s Governing Council determines the strategy within the framework of that mandate.

The ECB’s new monetary policy strategy was set out in a statement published on 8 July 2021 by the Governing Council. The monetary policy strategy sets out how the ECB is to maintain price stability in the euro area and what goals it has established for its monetary policy. The strategy also outlines how the ECB’s Governing Council is to determine the central bank’s monetary policy and communicate this. The ECB published a large number of strategy review articles in late September.

The Bank of Finland was actively involved in the ECB’s strategy review process. It held various seminars and events to gather views; these were aimed at the academic community, civil society organisations, the general public, national parliaments and the European Parliament.

Through such events, the Bank of Finland’s aim is to raise the level of interaction between the ECB and citizens. It plans to hold similar events in the future, too.

Strategy revision prompted by the changing operating environment for monetary policy

Changes had occurred in the operating environment for monetary policy since the ECB’s Governing Council last revised the strategy in 2003. This was the key reason for revising the strategy in 2021.

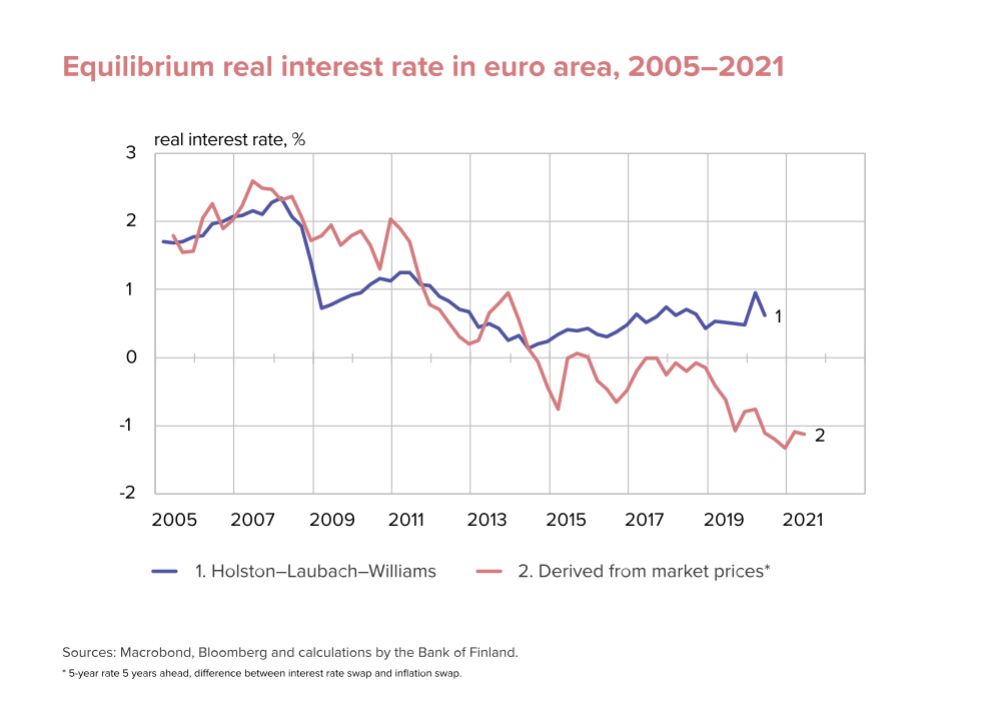

The long-term natural or ‘equilibrium’ real interest rate, i.e. the interest rate at which the economy grows in line with its potential and the inflation target is met, has decreased for structural reasons both in the euro area and globally (Chart 4). Estimates of the equilibrium interest rate vary and are subject to uncertainty.

One of the main structural reasons behind the decrease is the demographic transformation. The ageing of the population has boosted savings activity, increased demand for liquidity and reduced the level of interest rates. It may also have slowed GDP growth by impeding growth in productivity and investment.

Globalisation and the adoption of digital technologies have, in turn, had a long-term impact on the composition of goods and services production as well as the labour market, and perhaps also inflation. Furthermore, the ageing of the population has probably curtailed aggregate demand and thereby curbed inflation.

The financial environment has been substantially altered since the global financial crisis, and this has significantly affected the operating environment for monetary policy.

All the changes referred to above have limited the capacity of the ECB and other central banks to pursue any necessary relaxation of monetary policy by conventional means. In the economics literature this constraint is known as the zero lower bound for monetary policy.

ECB took climate change into account in its operational framework for monetary policy

Threats to environmental sustainability have emerged as key global challenges, and combating climate change has become one of the European Union’s main goals.

Climate change and the transition towards a more sustainable economy are visible in the macroeconomic indicators that measure inflation, total output, employment, interest rates, investment and productivity. They also have an impact on financial stability and monetary policy transmission. In addition, the influence of climate change and the transition to a lower-carbon economy will be felt in asset values and risk profiles on the Eurosystem balance sheet.

Although the main responsibility for tackling climate change lies with national governments and parliaments, the ECB considers it has a duty to take climate change considerations more effectively into account in its monetary policy operational framework, within the limits of its mandate.

The ECB is also expanding its analytical capacity in order to incorporate climate issues into its economic models and to promote climate change risk measurement and reporting. This will allow it to better acknowledge the risks involved in risk management, investment and monetary policy operations.

Diversity of ECB communications

Openness and accountability are essential for monetary policy to be clear and effective. To this end, the ECB will in future communicate its monetary policy through four different communications channels: a press release, a monetary policy statement, the Economic Bulletin and an account of the monetary policy meeting. In addition to these, the ECB will produce material aimed at the general public.

The ECB’s Governing Council also considered that in a rapidly changing world, the ECB’s monetary policy will likely need to be reviewed and adapted more regularly. The next assessment of the appropriateness of the monetary policy strategy is expected in 2025.

ECB inflation target 2%

The principal changes in the revised monetary policy strategy concern the price stability definition and the ECB’s inflation target.

For a long time, inflation was below the ECB’s price stability target, and this also reduced inflation expectations significantly. Inflation expectations were then no longer anchored to the ECB’s price stability target as strongly as before.

Under its new strategy, the ECB adopted a symmetric inflation target of 2% over the medium term. A symmetric inflation target means that the ECB’s Governing Council considers that both negative and positive deviations from this target are equally undesirable. This marks a significant shift in the ECB’s monetary policy.

The ECB’s de facto inflation target was distinctly below 2% prior to the new strategy, and its objectives in relation to inflation were asymmetric.

The ECB’s Governing Council also confirmed that the harmonised index of consumer prices (HICP) will continue to be an appropriate measure (Chart 5). The index measures the change in prices of goods and services purchased by households. The Governing Council also favours the future inclusion of costs related to owner-occupied housing in the index.

The symmetric 2% inflation target is unambiguous, clear and easy to communicate. It allows the ECB to focus on its capacity to maintain a sufficient safety margin against the risk of deflation and to make sure monetary policy has sufficient room for manoeuvre to respond to inflation that is too low.

It is also expected to influence long-term inflation expectations and to anchor them more firmly to the ECB’s target. Committing to a symmetric 2% inflation target removes the perception of a 2% upper limit associated with the inflation target as previously defined.

Price stability, balanced economic growth and full employment are mutually supportive economic policy objectives. The ECB’s strategy states that it aims for price stability over the medium term, and so this enables a monetary policy stance that is flexible in relation to different economic disturbances.

Governing Council took account of zero lower bound in its monetary policy

A persistent negative deviation in inflation is particularly detrimental because of the effective lower bound on interest rates and a low equilibrium real interest rate.

Commitment to the symmetric inflation target may require especially forceful or persistent monetary policy measures based on a thorough impact assessment if the euro area economy is at risk of drifting towards the effective zero lower bound.

If close to the effective zero lower bound, where a reduction in interest rates would do more harm than good, the ECB’s Governing Council would be ready to keep monetary policy accommodative for a longer period in order to stabilise the economy and inflation. This may also mean that inflation is above target for a transitory period.

Asset purchases, longer-term refinancing operations and forward guidance still part of the monetary policy toolbox

Central banks resorted to large-scale purchases of securities (Chart 6) and longer-term refinancing operations (LTROs) due to a decrease in the equilibrium real interest rate and because monetary policy is constrained by the zero lower bound. The aim was to halt the slowing of inflation.

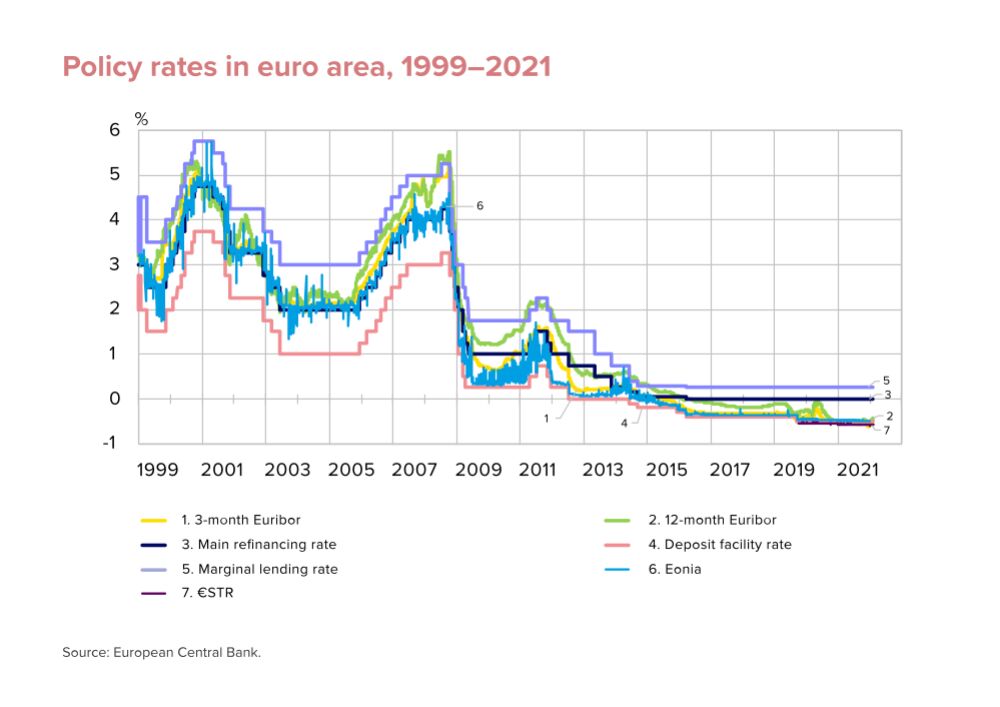

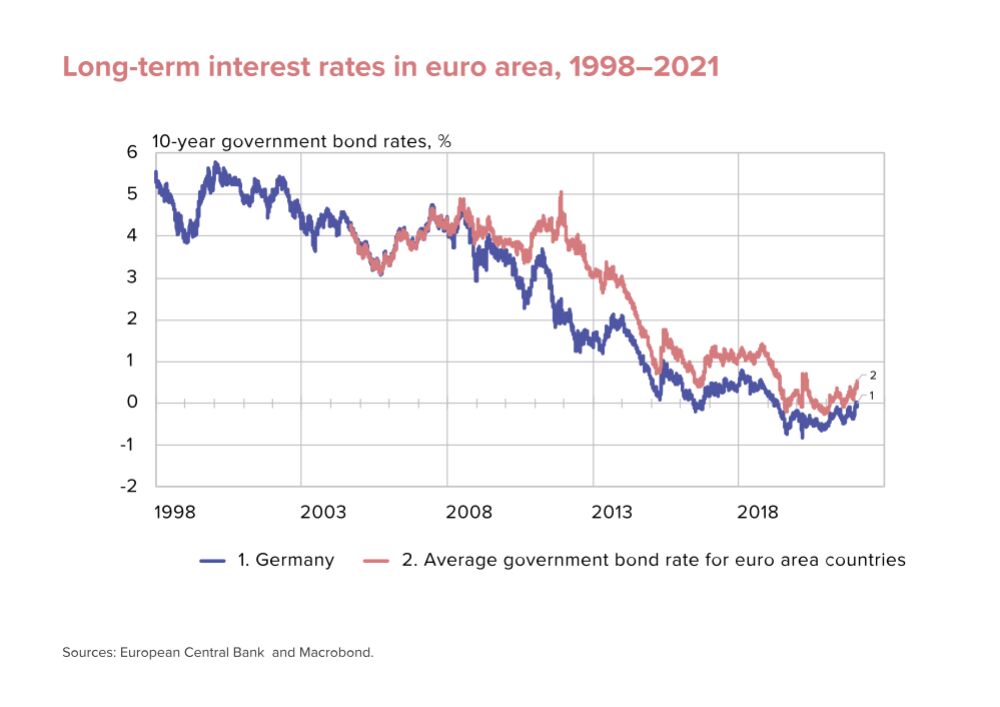

Interest rate policy was expanded into the realm of negative rates (Chart 7), and the impact of interest rate policy and the asset purchase programme on market rates (Chart 8) and the related expectations was intensified through decisions concerning the duration and amounts of measures. Bank lending and lending rates were influenced through targeted longer-term credit operations.

These new monetary policy instruments have had a significant positive effect on bank lending, GDP growth and inflation in the euro area. Use of the new instruments may nevertheless have its limits and can also have detrimental effects on financial stability, among other things. The Governing Council of the ECB will adjust the use of these instruments as necessary in order that second-round effects can be minimised, but without endangering price stability.

ECB’s monetary policy takes account of growth-stabilising fiscal policy

Fiscal policy operating on the principle of countercyclical economic policy may further the effectiveness of monetary policy during major recessions and when close to the effective zero lower bound. In such a situation, monetary policy and discretionary fiscal policy can mutually support and reinforce each other, underpinning recovery in the economy. The deployment of countercyclical fiscal policy nevertheless correspondingly requires buffers to be built up during upswings in the economy, if general government debt sustainability is to be secured.

Experience gained from the global financial crisis, Europe’s sovereign debt crisis and the global pandemic point to the fact that effective macroeconomic consolidation requires complementary fiscal and monetary policies during times of crisis.

ECB will continue to support EU’s general economic policies

The Treaty on European Union states that the primary objective of the European System of Central Banks (ESCB) shall be to maintain price stability.

Without prejudice to the objective of price stability, the ESCB will support the general economic policies of the European Union with a view to achievement of the objectives of the EU as laid down in Article 3 of the Treaty on European Union.

In deciding on the use of different monetary policy instruments, for example, the ECB’s Governing Council will endeavour to select the option which best supports the general economic policies of the EU. The Governing Council therefore also takes into account how the decision affects growth, employment, social progress and financial stability, and how it will help mitigate the effects of climate change.

Financial stability is a condition for price stability, and vice versa

Financial crises and instability are detrimental to economic growth, employment and investment. Financial stability is based principally on the responsible conduct of banks, investors and borrowers. Public authorities, through the regulation and supervision they pursue, seek to ensure that financial system risks remain under control.

When there is a disruption on the financial markets, monetary policy aimed at price stability will seek primarily to maintain liquidity in the financial system, prevent a weakening of bank balance sheets and lending capacity, and avoid debt deflation. In debt deflation, a fall in prices causes a rise in the real value of overall debt.

The primary responsibility for maintaining financial stability rests with the banking supervision and macroprudential policy decision-makers. Financial stability forms a flexible element of monetary policy that takes into account the prevailing circumstances, but without prejudicing price stability over the medium term. To this end, preparation of the ECB’s monetary policy decisions will include more extensive consideration of key factors affecting financial stability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}