Management of financial assets

5.3 Management of Bank of Finland’s financial risks

Implementation of monetary policy and safeguarding the stability and viability of the financial system are core central bank tasks. They involve financial risks, for which the Bank of Finland prepares by ensuring the strength of its balance sheet. In 2021, there was an increase in the risks associated with the Bank’s monetary policy and financial assets.

Risks arise in investment activities and the implementation of monetary policy

At the end of 2021, the Bank of Finland’s financial assets amounted to around EUR 11 billion. These consisted of gold holdings, foreign reserves and investments in equity and real estate funds. On the other hand, financial assets do not include items connected with the implementation of monetary policy, such as loans to banks or securities acquired in monetary policy operations.

Foreign reserves include liquid fixed-term investments. The amount of foreign reserves has been scaled to a level required in order for the Bank of Finland to perform its central banking tasks.

The domestic commercial papers acquired in 2020 in order to mitigate the adverse economic effects of the COVID-19 pandemic fell due in the first half of 2021. As a consequence, the Bank of Finland’s financial assets no longer included euro-denominated fixed-income investments at the end of 2021.

A significant proportion of the Bank of Finland’s financial assets are debt securities purchased for monetary policy purposes and claims on banks resulting from monetary policy implementation.

The Eurosystem’s monetary policy measures are implemented on a decentralised basis among the different Member States and the ECB, but, to a large extent, the risks and returns are shared among the national central banks.

The risk relating to monetary policy assets corresponds, in principle, to each national central bank’s capital key share in the aggregate monetary policy assets of the national central banks. At the end of 2021, the Bank of Finland’s share was 1.837%. However, the risks associated with government debt instruments and government-related debt instruments purchased under the public sector purchase programme (PSPP) and the pandemic emergency purchase programme (PEPP) are borne individually by each national central bank involved.

Increase in the volume of monetary policy assets

The volume of Eurosystem monetary policy assets grew in 2021 by around EUR 1,400 billion, reaching approximately EUR 6,900 billion by the end of the year. The increase was mainly due to the purchases of debt instruments under the PEPP and the loans granted under TLTROs (targeted longer-term refinancing operations). Furthermore, net purchases under the asset purchase programme (APP) continued in 2021, pushing up the volume of Eurosystem monetary policy assets.

The Bank of Finland’s share of monetary policy assets grew by around EUR 29 billion, reaching approximately EUR 119 billion by the end of the year. As a result of the increase in monetary policy assets, the risks associated with them also increased during the year.

| Table 7. | ||

| Bank of Finland’s financial assets and share of monetary policy assets | 31 Dec 2021 EUR million |

31 Dec 2020 EUR million |

| Financial assets | 10,946 | 10,010 |

| Gold | 2,537 | 2,434 |

| Foreign reserves | 6,720 | 6,261 |

| Euro-denominated fixed-income investments | 0 | 61 |

| Equity fund investments | 1,513 | 1,135 |

| Real estate fund investments | 176 | 119 |

| Share of monetary policy assets | 118,748 | 90,022 |

| Refinancing operations | 40,446 | 32,939 |

| Targeted longer-term refinancing operations1 | 40,375 | 32,423 |

| Other refinancing operations1 | 70 | 515 |

| Debt instruments under the asset purchase programme | 50,121 | 43,842 |

| Finnish government bonds and government-related bonds | 34,554 | 29,822 |

| Bonds of supranational institutions1 | 4,859 | 4,580 |

| Covered bonds1 | 5,019 | 4,841 |

| Corporate bonds1 | 5,688 | 4,600 |

| Debt instruments under the pandemic emergency purchase programme2 | 28,070 | 12,747 |

| Terminated programmes | 111 | 494 |

| Securities markets programme1 | 101 | 484 |

| Covered bond purchase programme | 10 | 10 |

| Total | 129,694 | 100,032 |

| 1) Capital key share (1.837% as of 1 Feb 2020) of aggregate claims by national central banks. 2) In the case of the pandemic emergency purchasing programme the table shows the amount on the Bank of Finland’s balance sheet. |

||

In addition to the claims listed in Table 7, the Bank of Finland's assets included EUR 34 billion in intra-Eurosystem claims, consisting mainly of the Target2 balance. At the end of 2021, the Bank of Finland’s balance sheet total was EUR 176 billion.

The Bank of Finland manages its risks through diversification

The Bank of Finland’s financial risks consist of market, credit and liquidity risks. Market risks include adverse movements in exchange rates, interest rates and stock prices.

Exchange rate risk is the source of most volatility in the value of the financial assets. The Bank of Finland diversifies its exchange rate risk by investing in the US dollar, the Pound sterling and the Japanese yen. The exchange rate risk is also diversified with investment in the Chinese yuan, since the Bank of Finland has receivables from the International Monetary Fund (IMF).

A strategic allocation of investments is determined by means of a benchmark index. This, together with a highly detailed limits framework, acts as a guide to taking on interest rate and credit risks. In this way, the Bank ensures that the investments are highly liquid and are adequately diversified across various asset classes, countries, maturities and issuers. The Bank’s investment focus is on debt securities with high credit ratings.

The Bank of Finland invests some of its own funds in a variety of instruments on the international stock and real estate markets. The investments are made through funds and diversify the other risks on the Bank’s balance sheet.

In the implementation of monetary policy purchase programmes, the Bank of Finland, in the same way as the other central banks, complies with the Eurosystem eligibility criteria and other risk-management rules.

The Bank of Finland manages its financial assets in a responsible manner. The counterparties accepted in direct fixed-income investments are delimited using specific responsibility criteria. Assessments of the responsibility and reliability of service providers are also essential in the Bank’s indirect investment activities.

Structural interest rate risk on the Bank of Finland balance sheet

The Eurosystem sets the interest payable on the central bank deposits made by commercial banks as a matter of policy. The interest rate decision has an immediate effect on the Bank of Finland’s interest expenses. Monetary policy assets, however, mainly carry a fixed interest rate. Thus, an increase in the deposit rate weakens the Bank’s net interest income. This difference in the interest rates applied to assets and liabilities on the balance sheet poses a structural interest rate risk for the Bank of Finland’s balance sheet.

Liquidity created via the purchase programmes and refinancing operations is reflected on the liabilities side of the balance sheet as growth in central bank deposits. The structural interest rate risk position decreases as the fixed-rate debt instruments acquired for monetary policy reasons mature.

As net purchases under the purchase programmes continue, the structural interest rate risk position increases. Furthermore, the reinvestment of principal payments from maturing bonds serve to maintain the structural interest rate risk position.

Quarterly updates on financial risk figures are available at suomenpankki.fi, under the section Risk management and control.

Increased risk associated with the Bank of Finland’s monetary policy and financial assets in 2021

The Bank of Finland’s balance sheet as well as the risk associated with monetary policy increased in 2021 in comparison with the previous year. The reason for the greater risk was mainly the increase in the volume of monetary policy assets, which was affected in particular by monetary policy stimulus measures. Furthermore, the risks attached to the financial assets increased slightly, mainly because of the rise in value of equity fund investments.

The Bank of Finland measures total risk exposure on the balance sheet using well established statistical methods. The risk estimate is supplemented with stress tests that assess losses that could be incurred under possible, though improbable, scenarios.

In estimating credit risk resulting from monetary policy assets, the Bank of Finland uses internal risk reporting produced by the ECB, which is subject to ongoing development by the Eurosystem’s Risk Management Committee.

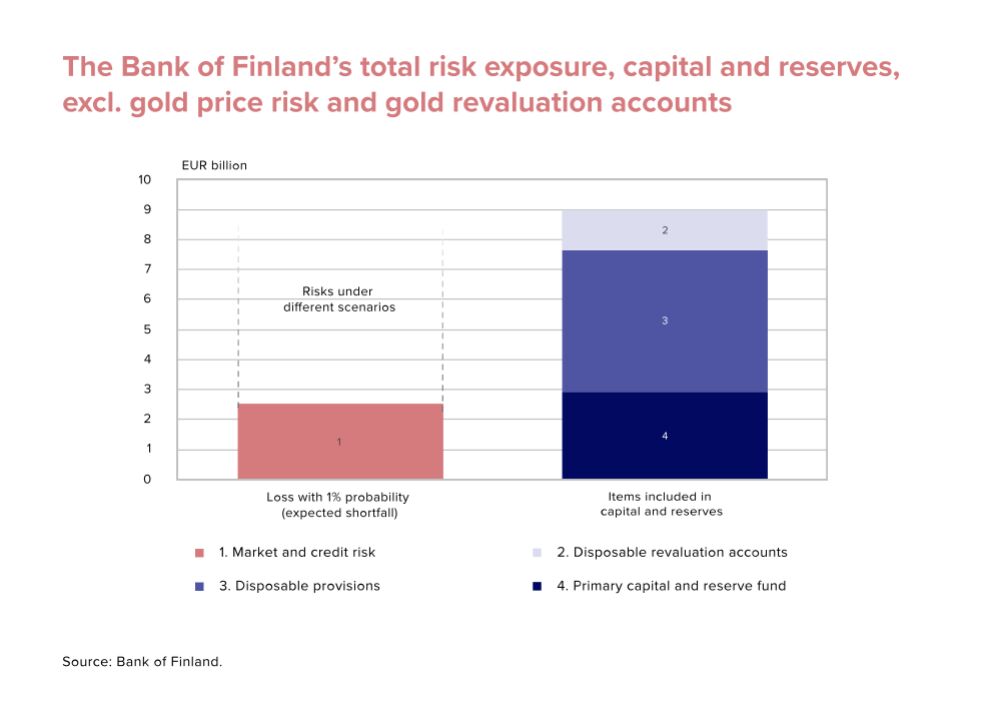

As the total risk estimate, the Bank of Finland uses a loss that would occur in the following year with a probability of 1% (expected shortfall).

At the end of 2021, the total risk estimate was EUR 2.5 billion. This figure does not include the gold price risk, as the gold revaluation accounts cover a significant decline in value. If the gold price risk is included, the total risk estimate is EUR 2.8 billion.

At the end of 2021, the Bank of Finland had revaluation accounts totalling EUR 1.3 billion and provisions totalling EUR 4.7 billion available to cover losses. The primary capital and reserve fund amounted to EUR 2.9 billion (Chart 27).

The risk buffers strengthened in 2021, largely as a result of currency fluctuations and the rise in value of equity fund investments.

The Bank of Finland’s capital adequacy is sufficient to cover the risks arising in the performance of its tasks (Chart 28).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}