Monetary policy

2.3 Monetary policy implemented with tools old and new in 2020

In 2020, the Eurosystem safeguarded favourable financing conditions and the availability of major currencies in the euro area as the COVID-19 pandemic devastated the economic outlook. It conducted its longer-term refinancing operations with more favourable terms and conditions; it eased the collateral requirements on its liquidity operations; it stepped up its monetary policy asset purchases; and it established swap lines with central banks. In addition, the Bank of Finland implemented certain domestic measures to support the availability of collateral for its monetary policy counterparties.

The Bank of Finland is responsible for implementing the Eurosystem's monetary policy in Finland. The Eurosystem implements its monetary policy with an assortment of tools that can be classified as standard and non-standard measures.

The Eurosystem's standard measures are its regular open market operations that it conducts as tender procedures against collateral; its standing facilities; and its minimum reserve system. Standard monetary policy measures primarily influence short-term market rates.

The Eurosystem's non-standard measures include, among others, its asset purchase programmes; its targeted longer-term refinancing operations; and its collateral policy. Non-standard measures have been at the centre of monetary policy since the global financial crisis and were all-important in the Eurosystem’s response to the challenges posed by the COVID-19 crisis in 2020.

Interest rates remained historically low in 2020

The Eurosystem's deposit facility rate, main refinancing operations rate, and marginal lending facility rate were held at their historical lows in 2020, at −0.50%, 0.00% and 0.25%, respectively (Chart 4).

The Governing Council reiterated throughout the year that it expects the key interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below 2% over the medium term.

In the current environment of ample excess liquidity, the deposit facility rate functions as the Eurosystem's main policy rate, as it influences the level of very short-term market interest rates.

The overnight reference rate €STR, as well as its predecessor the EONIA, which has since been fixed to the €STR, closely tracked the deposit facility rate throughout 2020. In spring, the emerging COVID-19 pandemic led to a spell of market panic, causing longer-term reference rates, such as the three-month and twelve-month Euribors, to momentarily rise by 0.3 percentage points, to about 0.0%.

However, following the Eurosystem’s comprehensive stimulus measures, the Euribors eventually fell to levels below −0.50% over the course of the year, reaching even lower levels than before the crisis.

Longer-term refinancing operations had their conditions eased, allowing for high take-up

Non-standard longer-term refinancing operations played a key role in the Eurosystem’s response to the COVID-19 crisis in 2020.

In December 2020, the Governing Council announced three additional operations to be conducted in 2021 under its third series of targeted longer-term refinancing operations (TLTRO III).

The interest rate applied on TLTROs is lower for banks that increase their net lending to households and non-financial corporations over a specified reference period.

The Governing Council eased the conditions of its three-year TLTROs multiple times in 2020. The maximum amount that counterparties are allowed to borrow under TLTRO III operations was raised twice: first, in March, to 50% of a counterparty’s eligible loan stock, and again, in December, to 55% of the eligible loan stock.

The eligible loan stock is based on a counterparty’s loans to non-financial corporations and households as at February 2019, excluding loans to households for house purchase.

The minimum interest rate on TLTRO III operations was also lowered for the next few years. In March 2020, the Governing Council decided that between June 2020 and June 2021 the interest rate applied on TLTRO III operations can be as low as 0.25 percentage points below the average interest rate on the deposit facility for banks that increase their net lending. In April, the Governing Council further reduced this to 0.5 percentage points below the average deposit facility rate, and in December it decided to apply the reduced interest rate on all operations outstanding between June 2021 and June 2022.

The Eurosystem has never previously granted central bank credit at an interest rate lower than the ECB's deposit facility rate.

In the early stages of the pandemic, the Eurosystem also conducted a series of additional longer-term refinancing operations to bridge the gap between TLTRO III operations, and it announced a new series of pandemic emergency longer-term refinancing operations (PELTROs). These operations were all conducted as fixed-rate tender procedures with full allotment.

The bridging operations were conducted on a weekly basis between 16 March and 8 June 2020, with all loans maturing on 24 June 2020 and issued at a fixed interest rate equalling the average of the deposit facility rate (−0.50%).

In May 2020, the Eurosystem launched its new series of monthly PELTROs. The PELTROs initially comprised seven additional refinancing operations maturing in 2021 and carried out as fixed rate tender procedures with full allotment, with an interest rate 25 basis points below the average rate on the main refinancing operations prevailing over the life of each PELTRO.

In December, the Governing Council announced four additional PELTROs to be conducted on a quarterly basis in 2021.

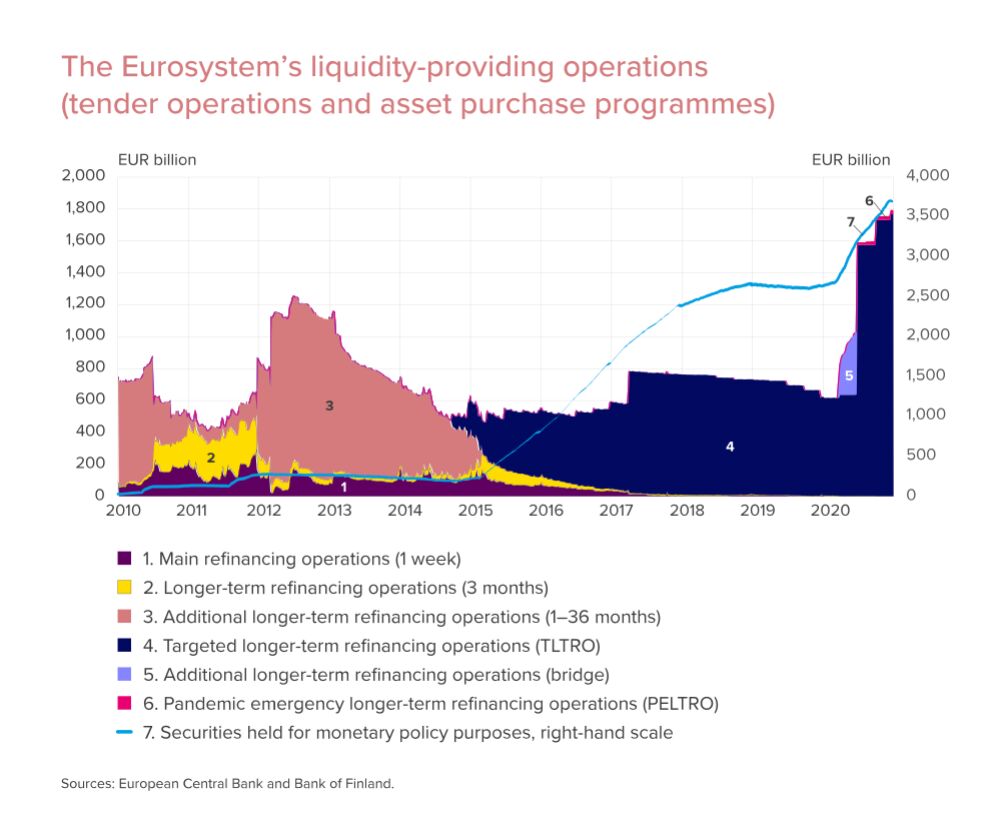

Banks have been especially active in participating in TLTROs. In 2020, the amount of outstanding Eurosystem liquidity-providing operations increased from about EUR 500 billion to over EUR 1,750 billion (Chart 5). This figure consists almost solely of TLTROs.

Similarly, the outstanding amount of bridging operations conducted in the spring peaked at almost EUR 400 billion. The number of participants in the Eurosystem’s operations has remained relatively high. For example, a total of 742 banks participated in the June TLTRO.

Availability of major currencies secured

Financial markets experienced a shortage of US dollar liquidity during the most tumultuous phase of the COVID-19 crisis in 2020. In March, the central banks of the United States, the euro area, Japan, Canada, Switzerland and the United Kingdom took action to coordinate a solution.

The ECB Governing Council decided to lower the pricing on its US dollar-denominated liquidity operations and began conducting these operations on a more frequent – and even daily – basis. It also began conducting US dollar-denominated operations with maturities of over 3 months, in addition to its one-week operations.

The Eurosystem procured the dollars needed for these operations through its swap lines with the Federal Reserve System, the US central bank.

The amount of US dollar-denominated refinancing held by Eurosystem counterparties peaked at over USD 140 billion during the spring. However, as the year progressed, the outstanding amount fell towards zero.

The Eurosystem also ensured that euro-denominated liquidity remained available outside the euro area during the crisis situation. It established swap lines with the central banks of Demark, Croatia and Bulgaria.

In addition, the Eurosystem established a backstop repo facility for non-euro area central banks (EUREP) and established bilateral repo lines with a number of other central banks.

Little to no demand for regular refinancing operations

The Eurosystem continued to conduct its weekly main refinancing operations (MROs) and regular three-month longer-term refinancing operations as fixed-rate tender procedures with full allotment. These operations are part of the Eurosystem’s standard monetary policy measures.

On 10 December 2020 the Governing Council confirmed that it would continue to conduct its regular lending operations as fixed rate tender procedures with full allotment, at the prevailing conditions, for as long as necessary.

In 2020, banks largely satisfied their liquidity needs by borrowing under the Eurosystem's longer-term liquidity operations and participated in its regular refinancing operations only sparingly.

The average outstanding amounts of MROs and three-month longer-term refinancing operations fell to about EUR 1 billion and EUR 2 billion, respectively.

The number of participants in the Eurosystem's regular liquidity-providing operations only declined over the course of 2020.

The liquidity surplus in the banking system grew even larger

The liquidity surplus in the euro area banking system, i.e. the amount of central bank reserves held by banks in excess of their minimum reserve requirements, increased by about EUR 1,700 billion in 2020, totalling about EUR 3,500 billion (Chart 6).

The rise in liquidity is explained, in particular, by the Eurosystem's increased pace of asset purchases due to the COVID-19 crisis and the higher take-up of TLTRO loans by banks.

The majority of the excess liquidity is remunerated at the ECB's (negative) deposit facility rate, but the two-tier system for remunerating excess liquidity introduced in October 2019 allows for an exempt tier to be remunerated at 0.00%.

The size of the exempt tier remained unchanged in 2020, at 6 times the volume of a bank's minimum reserve requirement.

Collateral easing in response to pandemic

The Governing Council made several adjustments to its collateral policy in 2020 to ensure that banks retain access to its refinancing facilities even in times of severe economic distress.

In April 2020, the Governing Council decided on a temporary expansion of the Eurosystem’s collateral framework. Among other measures, it reduced collateral valuation haircuts by a fixed factor of 20%, enabling banks to take more credit against the same collateral.

The Governing Council decided to relax the concentration limit for unsecured bank bonds as collateral, and it decided that marketable assets that met the eligibility criteria for collateral on 7 April 2020 would continue to be eligible in case of rating downgrades, as long as their rating remained at or above a specified threshold.

In addition, the Governing Council decided on an expansion of the additional credit claim (ACC) frameworks available to euro area national central banks.

On 10 December 2020, the Governing Council decided to extend the duration of its collateral easing measures to June 2022.

The Bank of Finland's domestic measures for ensuring the availability of adequate collateral

In addition to the Eurosystem's common collateral policy decisions, the Bank of Finland also implemented domestic measures to support the availability of collateral for its own counterparty banks and the flow of funding to firms and households.

On 1 September 2020, the Bank of Finland adopted an additional credit claim framework. This allows euro area national central banks to temporarily accept as collateral credit claims that do not fully satisfy the Eurosystem's common collateral criteria.

Under its ACC framework, the Bank of Finland accepts corporate credit claims as collateral that otherwise satisfy the Eurosystem’s general collateral framework but fall slightly short in credit quality.

The minimum credit quality requirement under the Bank of Finland's ACC framework is set at credit quality step 4 (BB+) in the Eurosystem’s harmonised rating scale, whereas the threshold under the general collateral framework is set at step 3 (BBB-).

Furthermore, the Bank of Finland’s ACC framework covers corporate loans that have been guaranteed by Finnvera Plc. The Bank of Finland has limited the guarantees accepted under the ACC framework according to, for example, their purpose and date of issue. This ensures that the eligible guarantees will be concentrated on corporate loans sought in response to the COVID-19 pandemic.

In addition, the Bank of Finland had already, on 1 April 2020, lowered the minimum threshold for credit claims for domestic use as collateral, from EUR 500,000 previously to EUR 25,000.

Substantial rise in collateral delivered to the Eurosystem

The overall volume of collateral delivered to the Eurosystem increased significantly (+47%) in 2020 due to the COVID-19 crisis (Chart 7).

The total amount of collateral deposited with the Eurosystem national central banks averaged EUR 2,294 billion in 2020, compared with EUR 1,562 billion on average in 2019.

There were some slight changes in the composition of collateral delivered to the Eurosystem in terms of asset classes. The volume of credit claims delivered as collateral increased, especially as national central banks implemented ACC frameworks and the haircuts on credit claims were reduced, consequently raising their collateral value.

Indeed, credit claims accounted for the largest share of collateral at 29%, with covered bank bonds and asset-backed securities coming in second and third, at 24% and 16%, respectively.

The Bank of Finland’s monetary policy counterparties remained unchanged

Credit institutions that are counterparties to Eurosystem monetary policy operations are subject to minimum reserve requirements and financial supervision and must be financially sound.

The Bank of Finland’s circle of monetary policy counterparties remained unchanged in 2020. At the end of the year, the Bank of Finland had a total of 16 counterparties. These consisted of both Finnish credit institutions and branches of Nordic banks operating in Finland.

Monetary policy counterparties may seek funding against eligible collateral by participating in the Eurosystem's credit operations.

Counterparties may also apply for overnight liquidity due for repayment the next bank day through the ECB's marginal lending facility, against eligible assets. Intraday credit, to ensure smooth payment flows, is similarly available against collateral.

The Eurosystem has specified eligibility criteria for assets that can be used as collateral in central bank credit operations. These criteria are outlined in the ECB's guidelines and are applied everywhere in the euro area.

In addition, the Bank of Finland has supplemented the ECB's guidelines with additional domestic requirements for its own counterparties. The Bank of Finland updated its provisions and guidelines twice in 2020. The latest provisions entered into force on 1 January 2021.

Bank of Finland counterparties held a record amount of central bank credit against a record amount of collateral

The amount of credit granted to Bank of Finland counterparties through the Eurosystem's liquidity-providing operations increased several-fold in 2020.

At the end of 2020, Bank of Finland counterparties held a total of EUR 21.8 billion in outstanding targeted longer-term refinancing operations (TLTROs), compared with EUR 4.6 billion at the end of 2019.

In addition to the Eurosystem's euro-denominated operations, Finnish banks participated in a number of US dollar-denominated operations in the spring. The outstanding amount of these operations peaked at slightly over USD 4 billion.

Counterparties also made use of intra-day credit.

The amount of collateral deposited by counterparties with the Bank of Finland reached a record high. The total amount of collateral deposited with the Bank of Finland stood at about EUR 27.4 billion, on average, in 2020, compared with EUR 17.2 billion in 2019.

The Bank of Finland's counterparties especially favoured covered bank bonds as collateral; their share of all collateral deposits increased to 42% (Chart 8).

The second largest share of collateral was accounted for by credit claims (30%), and the third largest by securities issued by central and regional government (14%).

The average amount of excess collateral from counterparties, i.e. the difference between the value of the collateral delivered to the Bank of Finland and the value of the credit provided, was about 51%.

The volume of deposits with the Bank of Finland grew in 2020

As in previous years, the Bank of Finland's counterparties held a significant amount of deposits with the Bank of Finland. The volume of deposits grew larger still in 2020 (Chart 9).

The volume of deposits stood at EUR 107 billion, on average, in 2020, compared with EUR 96.4 billion in 2019. Of this, only EUR 3 billion consisted of minimum reserves.

The Bank of Finland's overall share of excess reserves (deposits exceeding minimum reserve requirements) declined slightly in 2020, to about 4.1% of the Eurosystem's total excess reserves, on average.

Finnish banks made almost full use of their exempt tiers under the new two-tier system for reserve remuneration.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}