Financial stability

3.1 Companies’ ability to cope with the COVID-19 pandemic is important for financial stability

The Bank of Finland assesses risks and vulnerabilities that threaten the stability of the financial system. During the COVID-19 pandemic, the focus has particularly been on companies’ indebtedness and access to finance, and on future developments in banks’ credit losses.

The Finnish banking sector faced the COVID-19 pandemic with much stronger capital buffers than the financial crisis over ten years ago. In addition, the non-performing loans of Finnish banks have been at a very low level by European comparison for years (Chart 10).

However, one of the largest threats posed to banks by the pandemic is the increase in non-performing loans and credit losses as businesses face liquidity problems.

On the other hand, companies needed credit to cope with the loss of income, albeit in part temporary, caused by the pandemic.

In 2020, the Bank of Finland thus focused on monitoring corporate lending and on modelling and forecasting banks’ future credit losses.

Authorities cooperated in surveying companies’ access to finance

During the pandemic, the Bank of Finland enhanced cooperation with other authorities – particularly the FIN-FSA, the Ministry of Finance and the Financial Stability Authority – in monitoring the financial position of banks.

In March, the FIN-FSA, the Bank of Finland and the Ministry of Finance launched a regular survey of banks, which provided more information on the supply of finance to businesses.

The survey provided valuable information, particularly during the first months of the pandemic, on the funding needs of non-financial corporations and on the banks’ ability to respond to the need. The survey also quickly provided data on interest-only periods granted to non-financial corporations.

In 2020, the Bank of Finland analysed the indebtedness of domestic non-financial corporations and their debt-servicing capacity. The effects of the pandemic were distributed unevenly between sectors.

A sectoral analysis enables a more comprehensive assessment of indebtedness in the sectors that were hit most in the first phase of the pandemic.

The sectoral analysis also provides a more detailed picture of the financial position of the companies that are vulnerable in the structural changes accelerated by the pandemic, with for example teleworking and online shopping increasing.

As part of this analysis, the Bank of Finland also examined the sector breakdown of banks’ lending and how indebted the borrowers are.

Credit losses caused by the COVID-19 pandemic gradually accumulating

In spring 2020, the Bank of Finland prepared scenarios on probable developments in credit losses.

The credit loss model utilised two scenarios of possible trajectories of economic growth, prepared by the Bank of Finland’s Monetary Policy and Research department.

These scenarios were based on the assumption that Finland's GDP would contract sharply in 2020 due to the pandemic, but that economic growth would recover in 2021 and 2022.

The weak outlook for the economy was reflected in the assumptions also as a decrease in the value of securities and real estate. Even though the virus hit the economy hardest in 2020, credit losses would accumulate further in 2021 and 2022, as companies’ liquidity problems will be reflected in credit losses only with a lag.

As the pandemic progressed, the Bank of Finland also closely monitored the liquidity and funding positions of domestic banks. Despite the difficult market situation, particularly in the spring, the banks’ funding position eased already before the summer.

Work on borrower-based macroprudential measures continues

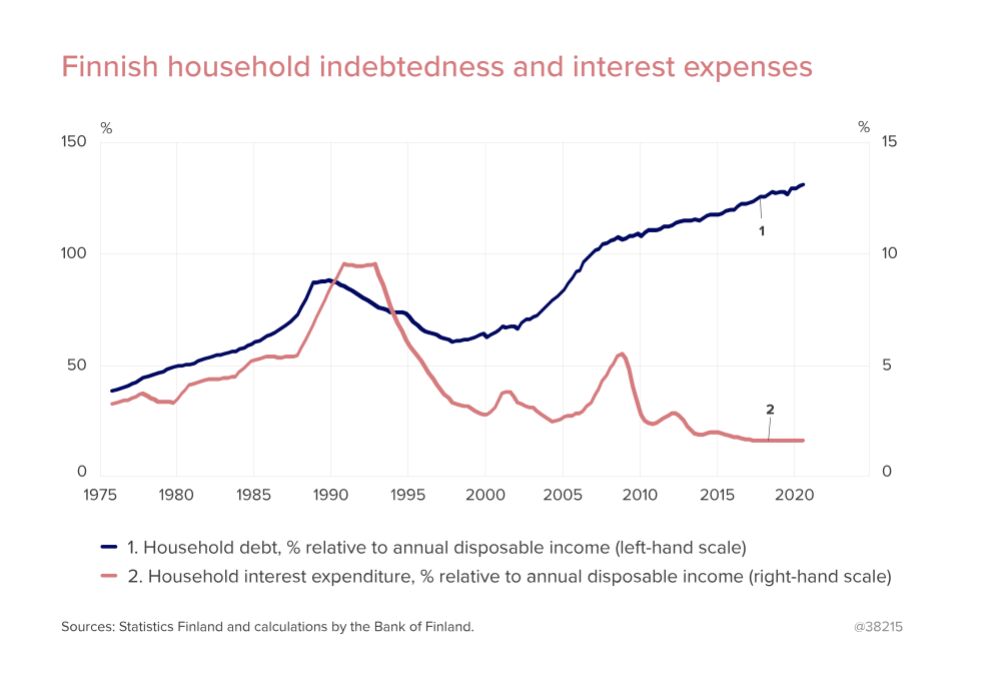

The Bank of Finland has for a long time expressed concerns about the increase in household debt (Chart 11). In 2018 and 2019, the Bank participated actively in the Ministry of Finance working group on new borrower-based macroprudential measures (Finnish).

In 2020, the Bank of Finland continued the analysis by, for example, monitoring the debt-to-income ratios of new housing loan borrowers.

The focus was also on estimating the appropriate maximum loan amount relative to the borrower’s annual income (maximum debt-to-income ratio) in Finland.

The Bank also modelled the effects of borrower-based macroprudential measures on economic growth.

If households have high debt-to-income ratios, a weakening of economic growth and rise in unemployment could force households to cut their spending.

If, on the other hand, the debt-to-income ratio is lower, the impact on spending could be smaller, which in turn would support economic growth.

In 2020, the Bank of Finland participated in the preparations for a positive credit register. The initiative is part of the government’s measures to curb excessive debt and, from the perspective of financial stability, the register will enable a more comprehensive and reliable monitoring of the credit market.

The Bank of Finland has emphasised that it is important that the credit register include also households’ exposures to housing company loans. The importance of these loans has increased in recent years, particularly in new-build construction (Finnish).

International macroprudential analysis focused on the housing market and banks

The Nordic banking sectors are interconnected, and the Bank of Finland has recognised the vulnerabilities related to this interconnectedness for a long time.

In all the Nordic countries, banks typically have large volumes of housing loans in their portfolios, and therefore a steep decline in housing prices could increase their credit losses.

The Bank of Finland has monitored developments on both the domestic and the Nordic housing markets during the crisis.

Despite the notable dip in the number of housing transactions in spring, the markets recovered rapidly. Towards the end of the year, housing prices rose in the other Nordic countries (Chart 12).

The Finnish banking system is also interconnected with the financial system of the entire euro area. The Bank of Finland has closely monitored the position of banks in the other euro area countries during the pandemic.

An additional focus was on the global financial markets – particularly on the United States, where non-financial corporations’ demand for debt was very strong in 2020.

The Bank of Finland also monitored and analysed growth in sovereign debt and the effects the growth could have. Most countries had to increase borrowing in 2020 in order to finance their economic support measures that were introduced in response to the pandemic.

The Bank of Finland's Financial Stability and Statistics department mainly participated in the work streams that assessed the interaction between macroprudential policies and monetary policy, as well as the impact of low interest rates on the transmission of policy decisions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}