Monetary Policy

1.2 Implementation of monetary policy in the euro area and Finland

In the Eurosystem, the national central banks implement the monetary policy decisions of the ECB Governing Council in a decentralised manner. Regular market operations conducted as tender procedures, standing facilities, and a minimum reserve system constitute the traditional part of the operational frameworkhttps://www.suomenpankki.fi/en/monetary-policy/implementation-of-monetary-policy/monetary-policy-instruments/.. The expanded asset purchase programme and a series of targeted longer-term refinancing operations have, in recent years, been key instruments for the implementation of monetary policy.

The Bank of Finland is responsible for the implementation of monetary policy in Finland. Credit institutions located in Finland hold current accounts with the Bank of Finland and may participate in monetary policy operations through the Bank. In addition, the Bank of Finland has also carried out a share of the Eurosystem’s outright transactions under the asset purchase programme.

Net asset purchases carried out until the end of 2018

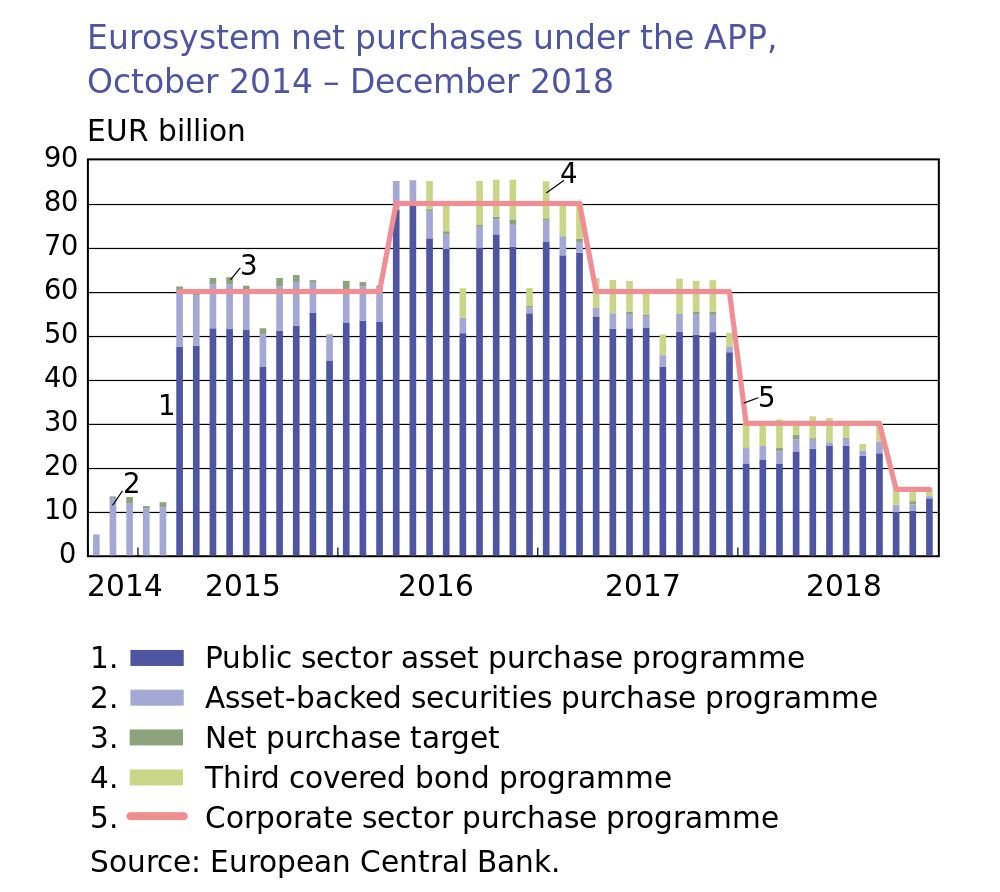

The Eurosystem's expanded asset purchase programme (APP) consists of the public sector purchase programme and three private sector purchase programmes, namely, the asset-backed securities purchase programme, the corporate sector purchase programme, and the third covered bond purchase programme.

In 2018, the target volume of monthly net purchases under the APP stood at approximately EUR 30 billion between January and September. This target was reduced to EUR 15 billion between October and December. In addition to its net purchases, the Eurosystem reinvested the principal payments from maturing securities purchased under the APP. These redemptions came to an average EUR 12 billion per month in 2018.

On the Eurosystem’s balance sheet, holdings of assets purchased under the APP increased from EUR 2,286 billion to EUR 2,570 billion during 2018. Holdings under the public sector purchase programme increased by EUR 213 billion, while holdings under the three private sector purchase programmes increased by EUR 70 billion.

In accordance with the ECB Governing Council's decision, net purchases under the APP ended in December 2018. As of 2019, the purchase programmes transitioned into the reinvestment phasehttps://www.eurojatalous.fi/fi/blogit/2018/eurojarjestelman-osto-ohjelmat-jatkuvat-uudelleensijoitusvaiheessa/.. Under the reinvestment phase, asset holdings no longer increase but are instead maintained at their current levels for an extended period. The volume of maturing assets is significant, with average monthly redemptions of about EUR 17 billion in 2019.

The Bank of Finland has made asset purchases under all of the programmes except the asset-backed securities purchase programme. In 2018, the Bank's balance sheet holdings of assets purchased under the APP increased from about EUR 38 billion to more than EUR 44 billion.

The Bank of Finland carries out a share of purchases under the corporate sector programme on behalf of the entire Eurosystem

At the end of 2018, the Bank of Finland's balance sheet holdings of sovereign bonds and bonds issued by European supranational institutions reached EUR 28 billion and over EUR 3 billion, respectively. Holdings under the private sector purchase programmes, in turn, reached almost EUR 13 billion at the end of the year.

Under the public sector purchase programme, the Bank of Finland supplemented its purchases of Finnish sovereign bonds and bonds issued by recognised agencies in Finland with bonds issued by European supranational institutions, as the sovereign bond purchases were not enough to fulfil the Bank's obligations under the ECB’s capital key.Under the public sector purchase programme, 90% of purchases are sovereign bonds and bonds issued by recognised agencies as well as regional and local governments, while the remaining 10% are bonds issued by European supranational institutions. Purchase volumes of sovereign bonds and bonds issued by recognised agencies as well as regional and local governments were determined by the capital key, reflecting each country's relative size to the entire euro area. According to the capital key, Finland's share was 1.78%. Under the third covered bond purchase programme, the Bank of Finland specialised in the markets for Finnish covered bonds.

Under the corporate sector purchase programme, the Bank of Finland operates as one of six euro area national central banks tasked with making purchases on behalf of the entire Eurosystem. In addition to buying Finnish corporate bonds, the Bank’s asset purchases included bonds issued by Irish, Austrian and Baltic corporations. These bonds were purchased from the Bank’s domestic and foreign securities-trading counterparties.

Securities lending followed as in previous years

Securities lending of assets purchased under the APP continued as in previous years. The aim of securities lending is to support bond-market liquidity in the euro area. The applicable holdings are made available for lending in a decentralised manner within the Eurosystem.

The Bank of Finland’s holdings were available for lending against securities as collateral through Euroclear Bank’s Securities Lending and Borrowing and GC Access services (see for further detail). In addition, the Bank of Finland also carried out bilateral securities lending of assets purchased under the public sector purchase programme, against cash collateral.

Volume of outstanding longer-term refinancing still considerable

Voluntary repayments of the Eurosystem's second series of targeted longer-term refinancing operations (TLTRO-II) began in June 2018, in accordance with the ECB's pre-announced repayment schedule.

The four-year TLTRO-II operations were part of the comprehensive stimulus measures announced by the ECB Governing Council in 2016. Under TLTRO-II, the Eurosystem, through its national central banks, offered counterparties affordable longer-term funding against collateral. In return, participating counterparties were expected to increase their lending to euro area households and firms.

In the four operations, which took place between June 2016 and March 2017, participating banks were allotted a total of EUR 740 billion. Voluntary quarterly repayments began two years from the settlement of each operation. By the end of 2018, outstanding TLTRO-II loans stood at EUR 719 billion, as banks sparingly acted on the opportunity for early repayment.

Before the start of the voluntary repayments, fixed interest rates on the refinancing operations were determined for each bank, based on the bank's success in raising its private-sector lending. At its most affordable, counterparties received funding with a four-year maturity and an interest rate fixed at the ECB's deposit facility rate, which was -0.40%. At the upper end, interest rates on TLTRO-II loans are capped by the ECB's main refinancing operation rate, at 0%.

Little demand for regular open market operations

The Eurosystem continued to conduct its regular one-week main refinancing operations and three month longer-term refinancing operations as fixed-rate tender procedures with full allotment. In October 2017, the ECB Governing Council had decided to continue to conduct its regular open market operations as such at least until the end of the last reserve maintenance period of 2019. The interest rate on the main refinancing operations remained at 0.00% in 2018.

Liquidity remained abundant in the euro area banking sector, owing to the effects of the expanded asset purchase programme, the TLTRO-II operations, and earlier monetary policy purchase programmes. Banks’ displayed only a slight appetite for credit from the Eurosystem's main refinancing operations, and even less than in 2017.

Outstanding credit under the main refinancing operations stood at about EUR 3.6 billion, compared with EUR 13.4 billion in 2017. The number of participants in these operations remained below 50. Similarly, demand remained low for the monthly three-month longer-term refinancing operations. Overall, the sum of outstanding loans under the three-month longer-term refinancing operations stood at about EUR 6.3 billion, compared with EUR 7.9 billion in 2017. The number of participants in these operations occasionally dipped below 20.

The Eurosystem continued its one-week US dollar-denominated liquidity providing operations in 2018. This procedure is based on a swaps arrangement between the Eurosystem and the US Federal Reserve. This refinancing instrument, initiated during the financial crisis, has seen minimal uptake, barring some exceptional periods.

Shortest money-market rates held steady by even and abundant excess liquidity

In 2018, the amount of excess liquidity in the euro area banking system reached a high of about EUR 1,900 billion (Chart 3). Because of the consistent abundance of surplus liquidity, the shortest money market rates in the euro area held themselves closely aligned with the ECB's deposit facility rate, which remained at −0.40% in 2018. The EONIA rate, which represents the overnight unsecured interbank lending rate, stayed at about −0.36% and within a narrow range of −0.37% to −0.34%.

Progress made in preparation of the new €STR benchmark rate

The Bank of Finland has been closely involved in the meticulous design of the methodology and other technical aspects of €STR (Euro Short Term Rate), the ECB's new overnight benchmark rate.

The methodology for calculating €STRECB: ESTER methodology and policies. was settled upon and publicised in 2018. The benchmark rate is based on banks’ statutory statistical reporting of their money-market transactions. The design process received considerable support from two public consultations, where industry representatives shared their own views.

ESTER is due for daily publication starting in October 2019. The new benchmark rate will immediately occupy an important position. In September 2018, the private-sector working group recommended ESTER as an alternative risk-free benchmark rate for the euro area and as a replacement for the EONIA ratehttps://www.eurojatalous.fi/fi/blogit/2018/ekp-n-tuleva-viitekorko-ester-on-toimialan-suositus-eonian-korvaajaksi/..

Strict eligibility criteria for monetary policy counterparties

The pool of the Bank of Finland's monetary policy counterparties increased by one, making for a total of 16 counterparties by the end of 2018. The Bank’s counterparties include both Finnish credit institutions and Nordic banks with branches in Finland.

Credit institutions that serve as counterparties to the Eurosystem's monetary policy operations are subject to minimum reserve requirements and financial supervision and must be financially sound.https://www.suomenpankki.fi/en/monetary-policy/implementation-of-monetary-policy/counterparties/.

Monetary policy counterparties may seek funding against eligible collateral by participating in the Eurosystem's credit operations. Counterparties may also apply for overnight liquidity, through the marginal lending facility, against eligible assets. Intraday credit, to ensure smooth payment flows, is similarly available against sufficient collateral.

The Eurosystem has specified eligibility criteria for assets that can be used as collateral in central bank credit operations. These criteria are outlined in the ECB's guidelines and are applied everywhere in the euro area.https://www.suomenpankki.fi/en/media-and-publications/publications/instructions-and-rules/bank-of-finland-rules-for-counterparties-and-customers/. In addition, the Bank of Finland has supplemented the ECB's guidelines with additional domestic requirements for its own counterparties.https://www.suomenpankki.fi/globalassets/en/media-and-publications/publications/instructions-and-rules/counterparty/documents/implementation-of-monetary-policy-operations-and-collateral-management_en_16042018.pdf. It last updated its provisions and guidelines in April 2018.

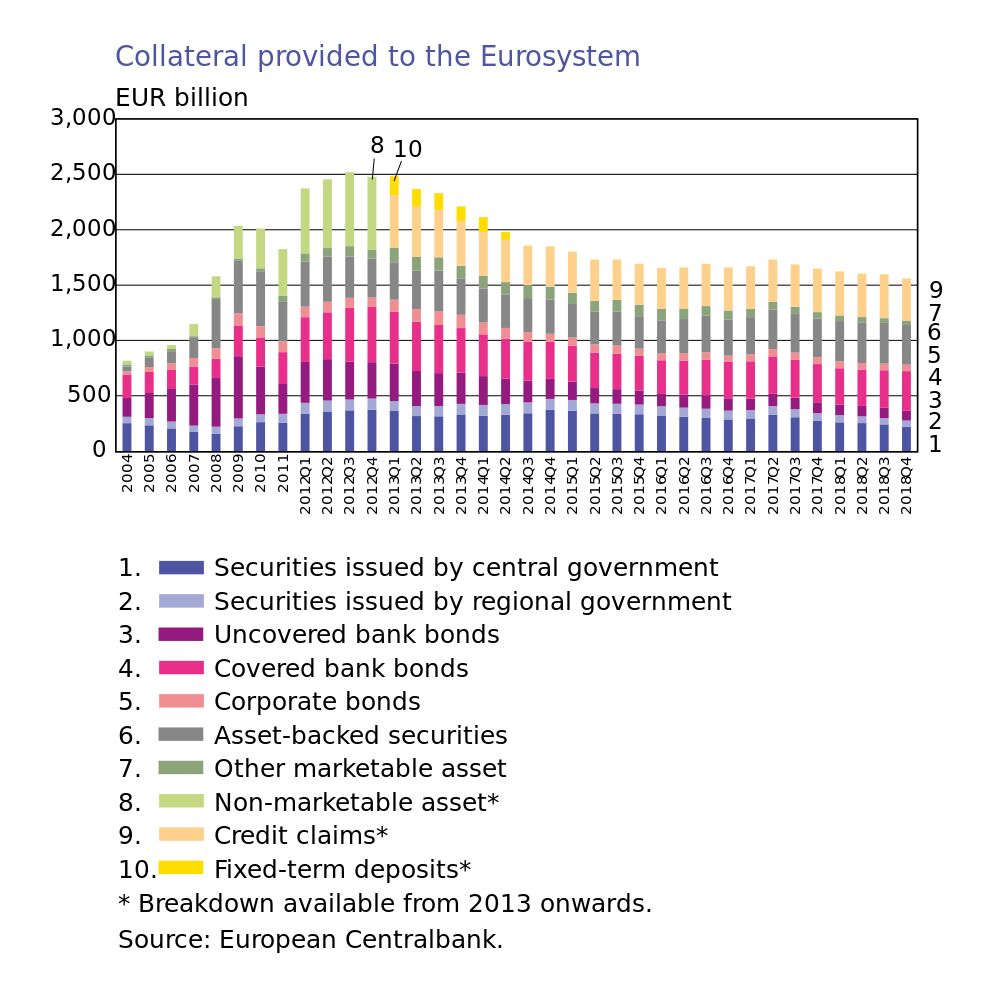

Slight reduction in collateral delivered to the Eurosystem

In order to receive credit from the Eurosystem's national central banks, counterparties must deliver collateral that satisfies the Eurosystem's eligibility criteria.https://www.suomenpankki.fi/en/monetary-policy/implementation-of-monetary-policy/collateral-for-central-bank-credit/.

In 2018, the total quantity of collateral delivered to the Eurosystem declined slightly (Chart 4). Overall, the Eurosystem's national central banks held EUR 1,594 billion worth of collateral in 2018, compared with an average of EUR 1,682 billion in 2017.

No significant change occurred in the distribution of asset classes delivered as collateral. Credit claims (non-marketable claims on loans by counterparties to their corporate and public sector customers) constituted the most popular asset class, representing 24% of collateral delivered, followed by asset-backed securities (23%) and banks’ covered bonds (21%), respectively.

Bank of Finland counterparties’ situation stable

The Bank of Finland's counterparties may participate in the Eurosystem's credit operations against sufficient collateral. In 2018, the Bank of Finland received an average of EUR 19.6 billion in collateral from its counterparties, compared with EUR 20.4 billion in 2017.

Bank of Finland counterparties continue to favour banks’ covered bonds as collateral, which on average accounted for 37% of all collateral delivered (Chart 5). This was followed by credit claims (29%) and bonds issued by central and regional governments (18 %).

Overall, the Bank of Finland’s counterparties reduced their financing from Eurosystem monetary policy operations. This resulted in counterparties’ collateral surpluses increasing to 27% in 2018, up from 26% in 2017.

The Bank of Finland's counterparties sought exceptionally little newly issued central bank liquidity in 2018, mainly opting to use intraday credit. By the end of 2018, the Bank’s counterparties held EUR 8.6 billion worth of outstanding credit received from targeted longer-term refinancing operations (TLTRO-II). A year earlier, this figure had stood at EUR 10.1 billion.

Voluntary TLTRO-II repayments began in June 2018, and the Bank of Finland's counterparties had made repayments of EUR 1.5 billion by the end of the year.

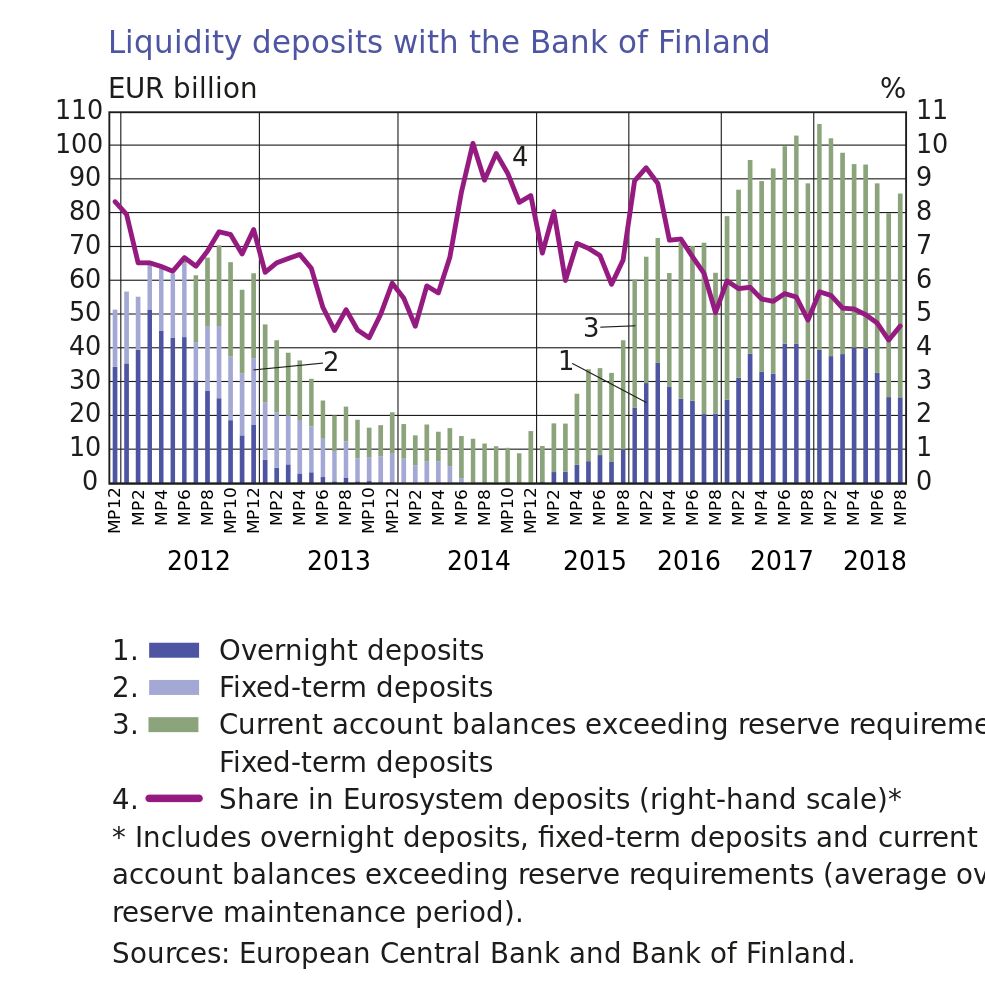

Central bank deposits grew in volume and shrank proportionally

As in previous years, the Bank of Finland's counterparties made a considerable amount of deposits with the central bank. Counterparties can either deposit funds using the actual overnight standing facility, or they can simply leave funds in excess of the minimum reserve requirement on their current accounts with the central bank. In either case, the Bank of Finland offers the same remuneration on these funds, equal to the ECB's deposit facility rate, which remained negative (-0.40%) in 2018. Remuneration is also paid on the minimum reserve requirement, corresponding with the main refinancing operations rate, which remained at 0.00% in 2018.

Excess liquidity, or the total volume of central bank deposits made with the Bank of Finland, averaged some EUR 94 billion in 2018. In 2017, this figure was EUR 92 billion (Chart 6). However, the Bank of Finland's share of central bank deposits within the entire Eurosystem shrank steadily in 2018, from almost 6% to under 5%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}